Welcome

Welcome to the September quarter news.

While noting the increased volatility of the past three weeks, investment returns for the most recent quarter echoed the previous June quarter. Some equity markets, including New Zealand’s, performed well, while some performed poorly.

The recent volatility in both local and overseas share markets may have impacted the value of your investment. This will depend on your chosen investment strategy. Volatility is a characteristic of investing in shares, an asset class that is expected to deliver higher returns than cash and bonds over the longer term (for example, more than 10 years). It is therefore important that your investment strategy suits your willingness and ability to take on the ups and downs. If you have any questions, please reach out to our contact centre on 0800 27 87 37.

See how your own investment strategy has performed:

Our regular My Future Strategy update provides information (but not advice) on what to think about when considering your future strategy. Find out more about what investors with long, medium and short term goals should be thinking about.

Also in this edition:

- SuperLife investments seminars 2018

- Are you in the right investment options for your investment strategy?

- Turn your savings into an income in retirement - and stay invested

Market Update

Investment returns

While noting the increased volatility of the past three weeks investment returns in the September quarter echoed the previous June quarter. Some equity markets, including NZ’s, performed well, while some performed poorly. The NZ dollar again fell over the quarter, boosting the return on offshore equities and property (on an unhedged basis). The box below discusses currency and how this is managed in SuperLife portfolios. Like equities, fixed income (bond) performances were also mixed. NZ bonds performed well, whilst offshore bonds had a weak quarter. The best way to benefit from such mixed performances is maintaining a well-diversified portfolio – enabling it to benefit from strong markets, and to be cushioned from markets not doing so well.

Overseas shares in “developed” markets returned around 5% in their home currency terms (on a MSCI world index basis), and 7.5% in NZ dollar terms given the decline in our currency. Australian equities in the September quarter returned around 1.5% (S&P/ASX 200 Index), while NZ equities returned around 4.5% (S&P/NZX 50 Index). Property market performances were also generally solid over the September quarter. The NZ market was the standout, as reflected in the 5.7% return to the Smartshares NZ Property ETF. Emerging Market equity performances were weaker, with the MSCI EM index returning around 1% on a NZ dollar basis. Emerging Market equities face several headwinds - capital outflows as the United States (US) has tightened interest rates, concern over rising trade tensions (hitting the Chinese market in particular), and instability in some economies such as Turkey and Brazil. The silver lining to this is that with the soft performance Emerging Market equities are now seen as very good value, particularly compared to the high-flying US equity market.

SuperLife’s NZ bond fund returned around 1% for the quarter and 3.5% for the year. International bonds returns have been weaker, with the annual return around 1%. They’ve been hit over the year by (forward) interest rates increasing at a faster pace than expected. A lot of this has come down to the US economy performing very strongly. In contrast, expectations of future interest rate rises in NZ have fallen over the past year, helping to boost NZ bond returns.

The fortunes of these different markets is reflected in Superlife’s fund returns. The higher risk SuperLife60 to SuperLife High Growth portfolios performed well over the quarter, as did Ethica. In contrast, performance of the SuperLife Income and SuperLife30 portfolios was relatively soft given low fixed income returns. Over the past several years the classic risk return trade-off has been very apparent. The Superlife High Growth portfolio, which has no exposure to fixed income, has returned around 11% per annum over the past three years. At the other end of the spectrum, the SuperLife Income portfolio, which has no exposure to equity markets, returned 3.9%.

Currency management considerations

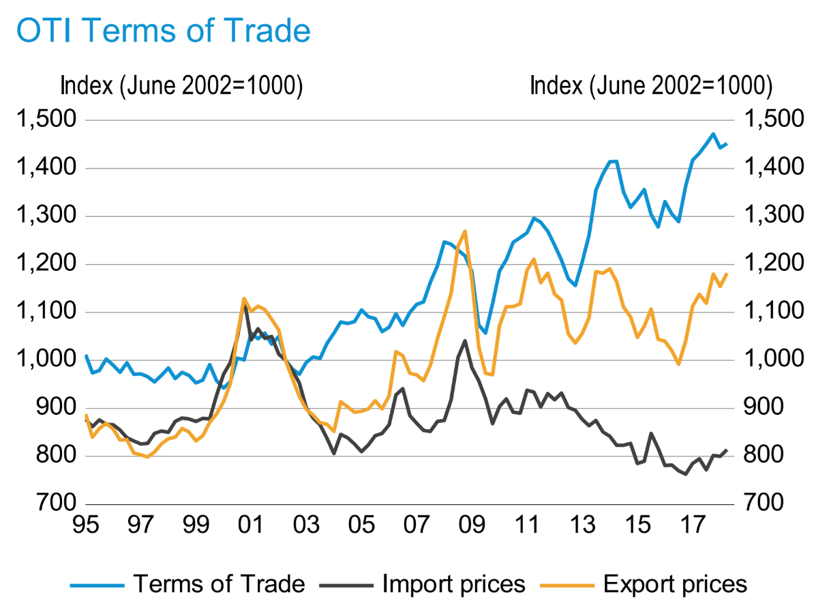

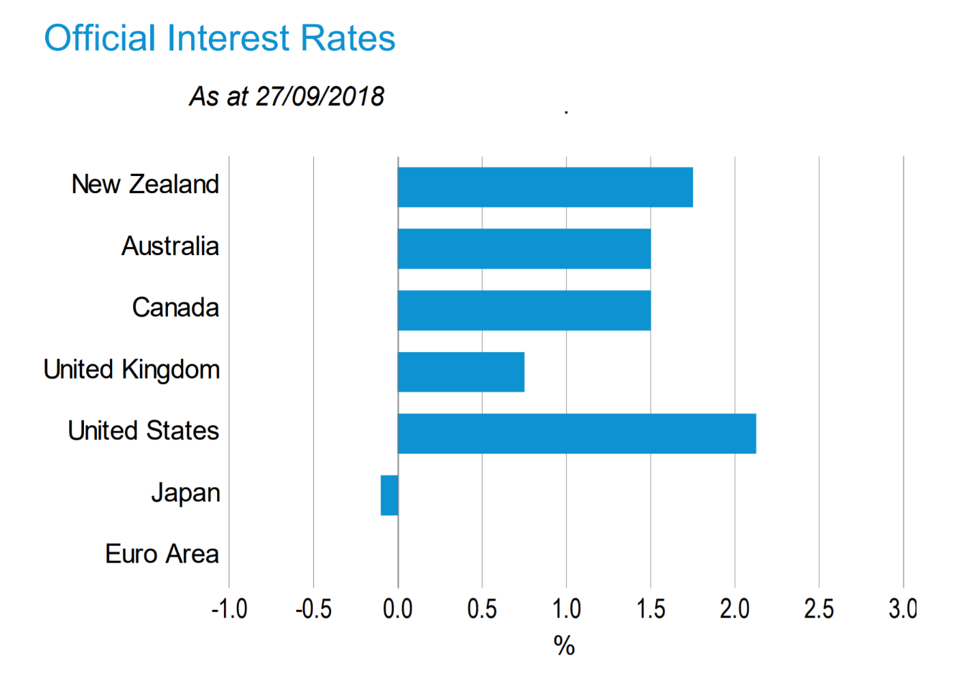

At around present levels the RBNZ estimates our currency is in the “goldilocks zone” - it’s supporting exporters and household spending and keeps our trade balanced. Through this lens the NZ dollar should stay put. But should is not the same as will – no one knows for sure where the currency will go from here. On the plus side our terms of trade (the price we receive for exports divided by the price we pay for imports) have climbed to record highs, and normally the New Zealand dollar follows this. However, the US cash rate is now 2.25%, well over our 1.75% overnight cash rate (see figure). Higher US rates favour currency speculators selling (shorting) the NZ dollar to buy US dollars, which could cause our currency to fall further.

While no one can accurately forecast short term currency movements, currency volatility can certainly be managed through currency hedging. In SuperLife portfolios much of the currency risk in offshore equity and fixed income holdings is reduced through currency hedging. An important reason for this is that most KiwiSaver investors care about the value of their portfolios in NZ dollars, and its ability to support a NZ-based retirement. Hedging offshore holdings helps ensure that, in the long run, investors will earn a premium over NZ cash from their investments, building up an asset base that can well-support a NZ retirement.

Also factored into the amount of hedging applied to Superlife Funds and their underlying building blocks are hedging costs, interest rates, and portfolio risk considerations. This leads us to fully hedge offshore fixed income, not hedge EM equities (where costs are typically very high), and to hedge around 75% of other offshore equity exposures. This means that investors will still get some portfolio diversification benefit when the NZ dollar falls, as it has over the past year or so.

Figure 1 NZ terms of trade are very high

Figure 2 But US interest rates lead the pack

My Future Strategy

For investors with long-term horizons, staying the course with your present investment strategy is usually the best option. This is subject to your goals, objectives and cash needs remaining broadly the same as when your strategy was established.

For investors with short-term cash needs, or who have taken more risk than they are normally comfortable with, the run up in markets over recent years presents an opportunity to increase cash holdings. While the global economic environment is currently robust downside risks are material. The International Monetary Fund recently cut its global growth outlook for the next two years given rising trade tensions and evidence this is starting to impact growth in China and elsewhere.

For investors concerned with performance over a medium-term horizon (next three to five years or so) there may also be an opportunity to enhance returns by tweaking your longer-term allocation to cash, bonds, equities and property stocks as follows:

- Holding less in bonds, and therefore more cash and shares. This reflects the view that interest rates may still increase more quickly than is currently factored into bond prices given the global growth and the potential for this to increase inflation faster than expected. Rising fuel prices and cost pressures present upside inflation and interest rate risk in NZ.

- Favouring corporate over government bonds, given the risk of faster interest rate increases is more material for government bonds.

- Favouring value, EM, Australian and European stocks compared to US and NZ stocks. These latter markets are broadly assessed to be more richly priced.

- Maintaining holdings of property stocks at around your long-term allocation.

- Maintaining the currency hedge on overseas shares at around your long-term allocation. We note that while short-term interest rates in the US are now higher than ours, NZ rates are still higher than foreign rates on a global market capitalisation (e.g. MSCI World Index) basis. This means hedging global equities will still earn investors a positive “carry”.

The strategy above doesn’t take into account an individual’s personal situation.

Also, as with all investment decisions, what might be the right strategy over the medium term, may not be right over the very short term. We really don’t know what will happen over the short term.

SuperLife investment seminars 2018

The SuperLife investment seminar series was recently held in locations across the country. Thanks to those of you that attended, as well as those that submitted questions for the speakers. We hope you found it informative and useful, and welcome your feedback for future seminars. If you were unable to attend a seminar in your region, please let us know if you'd like to receive a copy of the seminar presentation. This will also be uploaded to the SuperLife website in the first week of November.

Are you in the right investment option for you?

The right investment option or mix of investment options is unique to you. How you implement your investment strategy depends on your situation - in particular, how you feel about risk and volatility (ups and downs in the value of your investments), when you plan to spend the funds and what you might use them for (e.g. retirement or for a first home deposit). Read more on how to work out your investment option.

When you invest you must decide on an investment “strategy”. Your investment strategy is the mix of the different types of assets (i.e. cash, bonds, property and shares), in which your savings are invested. You should also decide how it should be changed over time. Your investment strategy is a major contributor to the returns you will receive from your investments and should therefore be designed to meet your financial goals. To learn more about this, read our Investment Guide.

The Government’s Sorted website also includes an “investor kick-start” page to help you think about what type of investor you are.

After you’ve thought about your investment strategy, you could then review SuperLife investment options to find an option to match. For a useful overview of SuperLife’s broad range of investment options visit our help me choose page.

SuperLife does not offer financial advice. You should see a financial adviser for advice specific to your circumstances. SuperLife has recently set up a free-of-charge facility enabling investors to agree a reasonable fee with their financial adviser and have it deducted from their investment account. For a list of financial advisers signed up in your region, please This email address is being protected from spambots. You need JavaScript enabled to view it..

Turn your savings into an income in retirement - and stay invested

When you reach retirement, and when it comes time to start spending your savings, SuperLife’s ‘managed income’ enables you to do that, while still remaining invested.

Managed income is an option where you manage how you draw down your savings in retirement. You can withdraw any amount you choose as often as you like, paid to your bank account, at no cost. You can stop, start, change the level of your withdrawal whenever you like. You can also take a lump sum at any time as well – it’s up to you.

This high flexibility, combined with SuperLife’s low fund charges, make it a good way to manage your money in retirement. You benefit as your savings can stay invested, in an investment option of your choosing, at the same time as you’re receiving an income.

You can continue to choose from SuperLife’s full range of investment options. For your chosen investment options that earn income (e.g. interest and dividends), you can have this income paid to the NZ Cash fund, so that it’s available when needed.

You can also rebalance your investment strategy, to maintain a minimum level of cash and/or bond investments. This helps reduce the risk of withdrawing money from shares and property funds at a time when the value of those funds has fallen.

Read our detailed article on managed incomes at www.superlife.co.nz/managed-incomes or phone 0800 278 737.

Smartshares Limited is the issuer of SuperLife Invest, the SuperLife KiwiSaver scheme, the SuperLife UK pension transfer scheme and the SuperLife workplace savings scheme. The Product Disclosure Statements and Fund Updates for these schemes are available at www.superlife.co.nz/legal-doc.