This SuperLife guide looks at family trusts. It is a general information guide only and cannot replace the specific advice you can receive from someone who understands trusts. It is important that you obtain appropriate legal, accounting and estate planning advice for your circumstances before making any decision on a family trust.

Key questions

When it comes to family trusts, you have to think about the key questions:

1. Should you have a family trust?

and if yes

2. How is a family trust established, and which is the best way to structure it?

3. What are the ongoing administration and management requirements?

A family trust should exist to achieve a person’s personal and family objectives. There should be a valid purpose. Also, the advantage of a trust to help achieve this purpose must outweigh the disadvantages of operating a trust. If there is an advantage and the expected benefits are greater than the costs, you should consider setting up a family trust. As everyone’s situation is different, decisions on your trust arrangements need to reflect your particular situation, though in practice, many of the decisions made will often be similar in principle, between one person and another.

In this guide

The advantages of a family trust

Family trusts

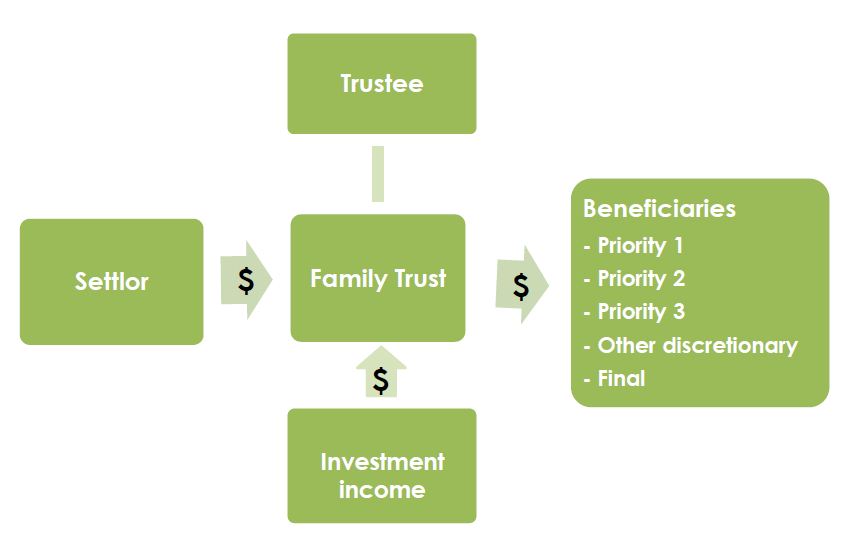

A trust exists when a person or a company (the settlor), gives money or assets (trust property) to another person (the trustee), to own, control and manage for the benefit of a third group (the beneficiaries) or for a specified purpose. The arrangements are governed by a set of tailored rules (the trust deed).

For most purposes, a trust is treated like a separate legal person. A trust can purchase and hold any type of assets. Income and assets owned by a trust are not the property of the trustee or the beneficiaries. The assets only become the property of a beneficiary when the trustee transfers or pays the assets from the trust to the beneficiary. As a result, trusts can be used to protect assets and distribute income from/or to other people.

A trust may be either “discretionary” or “fixed (non-discretionary)”. A beneficiary of a discretionary trust does not have a legal interest in the capital or income of the trust, until the trustee makes a decision to apply income or capital in favour of that beneficiary. A beneficiary of a fixed (non-discretionary) trust has specific entitlements to the trust funds on the basis detailed in the trust deed. Most family trusts in New Zealand are discretionary trusts, but it's possible for a trust deed to create both fixed and discretionary interests in the same trust.

A trust is therefore a relationship between:

- The settlor who creates the trust, says what the trust is for and what goes into the trust deed, and

- The trustee who holds the trust’s assets in its name (nominal owners) and has a legal obligation to deal with the assets as set out in the trust deed; and

- The beneficiaries who receive the benefits from the trust. The benefits may include a distribution of capital, a distribution of the income from the investments, or the use of the assets (e.g. a house). A family trust is where the beneficiaries are primarily family members. The beneficiaries may include:

a. Primary beneficiaries are distinguished from other discretionary beneficiaries and given priority above the other beneficiaries. There may be several layers (priorities) of primary beneficiaries. In some cases they are also final beneficiaries;

b. Discretionary beneficiaries who may receive a benefit from the trust at the discretion of the trustee. They only have the right to be considered for the distribution of income, capital or both, during the term of the trust;

c. Final beneficiaries who are entitled to receive whatever funds are still left in the trust when the trust is wound up. Usually they are also the discretionary beneficiaries.

The advantages of a family trust

The potential benefits from establishing a family trust, are normally one or more of the following:

- Protecting family members with special needs

- Creditor protection

- Protection against relationship property claims

- Protecting assets for future generations from law changes

- Eligibility for income/asset tested benefits

- Protecting property from being wasted

- Greater flexibility than a will

- Reducing or preventing family protection claims

- Tax saving on beneficiaries' income

- Confidentiality

- Insurance against future risks

Protecting family members with special needs

A family trust lets you put in place specific arrangements to look after a family member with special needs following your death. A family trust may also protect a child with special needs from other family members who may assume control of family assets when you die.

Creditor protection

Assets in a trust are usually protected from the beneficiaries’ creditors and the personal creditors of the trustees (if individuals) as assets belong to the trust governed by the trust deed.

There are some limits to the protections offered by a family trust arrangement. A trust cannot avoid claims from the IRD, business creditors and spouses/partners if those claims were subsisting when the family trust was established. If you are already subject to such claims, setting up a family trust will not protect you from those legitimate claims. However, family trusts are a legitimate way of protecting you and your family from new claims, which may be made against a beneficiary in the future.

If you are adjudicated a bankrupt any gifts made by you to a family trust within 2 years of your bankruptcy can be challenged by the Official Assignee under the Insolvency Act 2006. The Property Law Act 1952 also allows creditors to apply for a transfer of property to be declared invalid if it was transferred with the intention of defrauding them.

Protection against relationship property claims

If you transfer your assets into a family trust before you enter a relationship, the equal sharing rules under the Property (Relationships) Act 1976 will not apply and your new partner will not usually have any claim against those trust assets if you separate.

If you give assets to your children, those assets may become available to their partners under the relationship property legislation if they separate. A trust lets those assets be retained for the use of your children, on a break up of their relationship.

If your assets are owned by your trust or are given to your trust on your death, your children can continue to benefit from the assets and the assets do not form part of their personal property. They are therefore not subject to claims by their partners.

Protecting assets for future generations from law changes

Family trusts may provide protection against various forms of wealth tax e.g. death duties or inheritance tax which may be introduced in the future.

Eligibility for income/asset tested benefits

Government benefits, such as the widows' benefit and long stay residential/hospital care subsidies, are subject to asset testing. Assets held in a family trust are often not taken into account in assessing eligibility for such benefits. Family trusts may also offer protection against means testing of government benefits such as the sickness/invalid benefit.

Protecting property from being wasted

During your life or after your death through your will, you can simply give your assets to your children. However, not all children have the ability to manage their financial affairs. If you give assets to a family trust, the trust can provide for your children with income and/or capital to meet their legitimate cash and financial needs as they arise.

Greater flexibility than a will

You can leave your personal assets to a trust rather than directly to named family members when you die. This gives more flexibility than a conventional will. The trustee of a trust can then decide when to make payments to the trust’s beneficiaries and even whether to make such payments available at all.

Reducing or preventing family protection claims

The Court has no authority to rewrite your will to achieve parity but can effectively rewrite your will under the Family Protection Act 1955 if it considers that you have a moral and ethical duty to members of your family. In contrast, the Court cannot rewrite the provision of a trust in the same circumstances.

Tax saving on beneficiaries' income

Trusts are a separate entity for tax purposes and must file a return if they receive taxable income. Trust income is taxed in the following ways:

1. “Beneficiary income”. This applies where the trustee pays income to a beneficiary. The income is then treated as if the beneficiary had earned it themselves. The beneficiary’s income will be added to their other income and they will in most cases, be taxed at their personal tax rate. If the beneficiaries are not already receiving a significant income they may be able to take advantage of the lower rates of tax available to them.

2. “Trustee income”. This applies where the trustee retains the income in the trust. It results in a flat tax rate of 33%.

However, if the Commissioner of IRD believes that the only reason for creating the family trust is for tax avoidance, the Commissioner has the power, under the Income Tax Act 2007 to declare the trust arrangement as invalid and levy income tax as if the trust never existed.

Confidentiality

Family trusts are not publicly registered and the details of your family trust arrangements can therefore be kept confidential.

Insurance against future risks

In some cases no immediate financial benefit is achieved through a family trust. Often a trust is formed to reduce the impact of events that could occur such as: 1. claims from business creditors; 2. the need to apply for asset tested benefits (such as residential care subsidies); or 3. relationship breakdowns; 4. protection of a specific child’s needs on your death.

In these cases a trust can be compared with insurance against sickness, where an insurance premium is paid but no benefits arise if the insured does not get sick. For a family trust the initial set up cost and ongoing annual costs can be regarded as equivalent to insurance premium. However, there should still be a valid purpose for establishing the trust.

A trust may not provide any benefits if the risk that it was established for never arises, arises too soon before sufficient gifting has been completed or arises after the law has been changed so that the protection originally offered by a trust structure is no longer available.

The main potential disadvantages of a Trust include:

Loss of ownership

If you transfer your assets to a trust, the trustee of the trust owns the assets while you can retain some control by having the power to appoint and/or remove a trustee or to name additional beneficiaries, or even by being a trustee yourself, the assets in the trust are no longer your own. If you continue to treat the assets as your own, the trust could be open to challenge.

Costs

There are costs involved with setting up a family trust and transferring assets to it. The costs will depend on the complexity of the trust the advisors used and the nature of the assets to be transferred. There are also significant costs in maintaining a trust and complying with the trust deed, trustee obligations and legislation.

If you establish a trust you need to allow for the time and cost involved in doing the trusts’ annual accounting, gifting and administrative requirements.

Future law changes

Possible changes to legislation or trust law may limit the advantages gained in the context of the original objectives, or may increase the compliance costs.

Relationship property issues

If you currently live in a married, de facto or civil union relationship, it is likely that your personal assets will be relationship property. Under the Property (Relationships) Act 1976 if you and your partner /spouse separate, that relationship property must, except in limited circumstances, be divided “equally”. However, assets held by a trust are trust assets, not personal assets. As a result, they are normally not subject to the relationship property division. Transferring family assets to a family trust can have a significant impact on your relationship property rights.

It is particularly important for you to understand the impact of the relationship property legislation on your family trust arrangements:

1. In some cases, if your spouse/partner transfers assets to a trust, it removes the relationship property rights you may otherwise have been entitled to;

2. In some cases, where inappropriate payments or transfers have been made to a family trust, courts have the power to make compensatory judgments to the spouse/partner who has been disadvantaged by the trust arrangement.

It must be noted that the rights relating to relationship property will have precedence over the family protection claims under the Family Protection Act 1955.

Establishing a trust

The decision to establish a family trust will have a significant impact on the way you manage your family assets. It is therefore important that the trust is established to meet your needs today and to recognise that those needs may change. There are a number of important decisions.

- Who will be the trustee?

- Who will be the beneficiaries and what will be their priority?

- What should be the rules in the trust deed?

- What will be the trust assets?

The Trustee

The trustee holds legal title to the trust assets. It has the power, subject to the trust deed, to deal with those assets as it sees fit. As the trustee has control over the trusts’ assets, it is important that you choose the decision maker(s) carefully. If the trustees are individuals the only restriction is that they must be mentally capable and over 20 years of age. You can be a trustee and a beneficiary of a trust you establish so long as you are not the sole trustee and sole existing or potential beneficiary at the same time.

The traditional approach is to appoint 2 or 3 individuals including you, your spouse/partner and a friend or a professional advisor with skills and expertise useful to the management of the trust’s affairs, as an independent trustee. The independent trustee will improve the integrity of the trust. However, the best structure is normally to establish a company as the trustee and appoint 1, 2 or 3 people to be the directors. The company can be owned by you (and/or your partner). The directors of the company can include one or more independent people if appropriate. The advantages of a corporate trustee, is that there will be perpetual succession, ease of administration and reduces costs and also it provides greater control. These days the cost of establishing a company are low (under $200), can be done online and the ongoing costs are nil if reporting is done electronically.

As an alternative to appointing an individual independent trustee, some trust deeds provide for the appointment of an independent protector. An independent protector is not a trustee but for some important decisions such as capital or income distributions or variations to the trust deed their approval is required. The independent protector is not involved with the trust on a day to day basis, nor signs documents for the trust. This arrangement simplifies the administration of the trust if the alternative is to have individual trustee but retains the involvement of an independent person in major trustee decisions. However, it is not as efficient as having a company.

If you set up a trust, you can be a beneficiary as well as a trustee, though in most cases it is better to have an older relative establish the trust (be the settlor) and have a company to act as the trustee, of which you are a shareholder and a director. This separates out the rules of roles, trustee and beneficiary, and maximises control.

The beneficiaries

Anybody can be made a beneficiary of a trust if the trust deed contemplates them to be one. It is important to remember that discretionary beneficiaries do not have an automatic right to receive benefits from the trust; they only have a right to be considered by the trustee when the trustee decides to make benefits available. This means that the group of beneficiaries you choose should be wide enough to include people who you actually want to benefit from the trust, but not so wide that the trustee has to consider the needs of a large group. In contrast, specific beneficiaries may be given to specific rights to the benefits as described in the trust deed.

The most common groups of beneficiaries are immediate family, relatives, close friends, charities and other trusts established for the benefit of these beneficiaries. It is generally good to include a power to add further beneficiaries to the trust once it has been established, to ensure that it can meet your future circumstances.

In most cases, it is best to establish priority layers of discretionary beneficiaries. For example,

Priority 1 typically a couple

Priority 2 their children

Priority 3 the children’s children

Priority 4 other family members.

A final beneficiary may be a charity, should all prior beneficiaries die.

The trust deed

The trust deed is the document which sets out the rules for how the trust will be administered. It is the document that establishes the trust. The trust deed needs to be flexible reflecting your intentions for setting up the trust. Changing a trust deed once it has been signed is not always a simple matter. It is therefore very important to ensure that the trust deed is prepared correctly at the outset. However, in most cases, a large part of a trust deed will be in standard form.

The trust deed should give at least one person the power to appoint additional trustees and to remove any trustee from office. If you set up the trust you would usually have this power of appointment and removal.

The trust assets

The trust acquires assets which are given or sold to it, often by the original settler or by family members. Decisions have to be made on the assets to be settled. The details of transferring assets to the trust are explained on page 9.

Transferring assets

Once a trust is established, you can transfer your assets to the trust. Although you can transfer any assets, it is normally best to only transfer assets which are likely to increase in value. Remember, a transfer is a sale by you and a purchase by the trust.

A trust acquires assets that are given or sold to it. Assets given may be subject to gift duty though the current law in New Zealand does not impose gift duty. Usually the assets are sold to the trust at current market values to avoid any gift duty liability. As most trusts do not have cash to buy the asset, the sale creates a debt due to the seller equal to the purchase price. The debt is repaid by payments made from the trust income or capital or forgiven by a gifting programme. Until a debt is forgiven it is a personal asset and is thus available to creditors. It is only when the assets have been fully vested in the trust and there is no debt to anyone that the trust assets have full protection.

The only assets protected by a trust are therefore:

- The subsequent increase in value, if any, of assets transferred to the trust;

- The amount of any gifts made to the trust; and

- The amount of income earned by the trust from its assets, which has not been distributed to beneficiaries.

It is often important to begin the process of transferring assets to a family trust as soon as possible so that the process of completely gifting the resulting debt can be completed as quickly as possible.

Gifts can be made in cash or by forgiving all or part of an outstanding debt. If you die before forgiving the debt owed to you by the trust, you can forgive the balance of the debt in your will. A forgiveness of debt under a will, as with any other gifts under a will, is not liable for gift duty.

It should be noted that in 2011 the government abolished gift duty. Assets can therefore be given to a trust without the need to set up complicated gifting arrangements.

Wider implication of selling assets

If you are considering transferring investment assets such as a rental property to a trust, you should obtain advice from a tax specialist on the tax implications of the transfer. If you have claimed depreciation on your rental property you may become liable for the depreciation recovered if you transfer the property to the trust.

Administration of a trust

Once a trust has been established, it must be administered properly. A trust achieves its objectives by separating ownership of family's assets from your personal assets. If the trust is not administered properly to recognise this separation, the trust could be challenged as a sham trust by a creditor, relationship partner, the IRD or WIMZ (Work and Income New Zealand). If such a challenge succeeds, the benefits available through the trust structure will be lost.

General administrative requirements

In general, the trustee of a family trust should:

- Meet on a regular basis to review the investments and the needs of the beneficiaries;

- Be involved in all trust decisions and record the decisions in writing;

- Ensure that it complies with the legal obligations imposed on trustees;

- Ensure that the trust meets its income tax obligations such as filing a tax return if the trust receives income;

- Act impartially towards all beneficiaries; and

- To seek and take professional advice where appropriate to do so.

Investment obligations

Under the Trustee Act 1956, trustees have a duty to invest prudently and to "exercise the care, diligence and skill that a prudent person of business would exercise in managing the affairs of others". Although some trust deeds exclude or reduce these obligations, all trustees are still expected to exercise a reasonable level of responsibility and prudence in carrying out their responsibilities. Section 13E of the Trustee Act provides a useful guide as to the matters that a trustee has to take into account when exercising any power of investment in respect of investments as a whole, or any investments specifically, as far as they are appropriate to the circumstances of the trust.

A passive trustee who merely rubber stamps the decisions of co-trustees, could be exposed to claims by beneficiaries for losses incurred by the trust.

Trustee liability

Trustees are personally liable for all the debts incurred by the trust including tax liabilities. It is customary for the liability of independent trustees to be specifically excluded in loan documentation and for a settlor to personally indemnify them for any losses they incur as a result of their trusteeship, as long as they are not negligent.

Taxation obligations

The Trust must meet its taxation obligations. The trustee needs to resolve, within six months following the end of each financial year (i.e. usually before 30 September each year). how any income earned by the trust will be treated. The trust income can be:

- Distributed to all or some of the beneficiaries and taxed at their tax rate (there are some limitations for distributions to children); or

- Treated as trust income and taxed at the trustee rate (currently 33%); or

- A mixture of these two options.

If a resolution is not passed within the six months timeframe, the income will be treated as trust income and taxed at the 33% tax rate.

Estate planning

A family trust is often part of a-wider estate plan. It should be accompanied by:

- A will dealing with your personal assets, including any debt owed to you by the trust;

- A memorandum of wishes; and

- An enduring power of attorney document.

The wider estate plan may include multiple trusts for different beneficiaries and different types of assets.

Will

When you establish your trust you should ensure your will deals with:

- Your personal chattels;

- The debt owed to you by your trust (if any);

- The balance of your estate (which is often left to the trust), and

- Your powers to appoint trustees and beneficiaries under the trust deed.

Memorandum of wishes

It is also recommend that you have a memorandum of wishes. A memorandum of wishes provides useful guidance for the trustee who operates the trust after you have died. However, a memorandum is not binding on the trustee.

The memorandum details your intentions for the trust and in particular:

- How you would like the trust to operate after your death;

- How the trustee should deal with the trust assets; and

- How benefits should be made available to the beneficiaries.

Enduring power of attorney

You should also have an enduring power of attorney (“EPA”) covering your personal property (assets) and another EPA for your personal care and welfare. These documents give a third person (the attorney), the power to act on your behalf in relation to your personal care and welfare when you become mentally incapable. However, with an EPA for property you can choose whether it comes into effect straight away or only when you can no longer manage your affairs.

Multiple trusts

In some situations, establishing more than one trust makes sense. This is particularly useful: 1. Where there is a particular need to separate the ownership of a family's business assets from lifestyle assets, such as the family home; or 2. For couples where one or both partners have their own children from earlier relationships, setting up one trust for each partner and possibly a joint trust lets the interests of their own children be protected. However, each trust incurs its own costs.

Common questions

How long can a trust last?

The usual maximum period under the law is 80 years. At the end of the period, the trust is wound up. However, the trust deed can give the trustees discretion to wind up the trust at a earlier date than the date in the trust deed.

How can you access trust income?

Distribution of trust income is at the discretion of the trustee subject to the trust deed. The trustee may subject to the trust deed:

- Accumulate and retain within the trust all or part of the trust's income.

- Make distributions of income to one or more of the beneficiaries in any proportions.

- Credit income to the current account of a beneficiary within the trust. The income will then be taxed as the beneficiary’s income and will be payable to the beneficiary on demand.

How can you access trust capital?

Before the trust is wound up distribution of capital is usually at the discretion of the trustee. Capital can usually be paid to anyone or more of the discretionary beneficiaries. If you are a beneficiary of the trust, you can therefore receive distributions of capital if the trustee decides to make such a payment. Alternatively, if the trust owes you money you may be able to access the trust capital by demanding repayment of all or part of the outstanding loan (subject to the terms of the loan agreement).

Can you use a house owned by a family trust?

If your family trust owns a house then the trust can make the house available to you to live in, provided that you are a beneficiary of the trust. The trust can let you live in the house on the basis that you pay the rates, insurance premiums and other day to day outgoings in lieu of rent. This decision of the trustee should be recorded in writing and should be reviewed regularly as part of the trustee’s review of the trust's investment policies.

Can a trust carry on business and invest?

Most trusts give the trustee an unrestricted power to act as if the trust were a natural person with no limitation on what the trustee can or cannot do. Trusts can therefore conduct a business in the same way as a natural person. However, some care needs to be taken where a trust is conducting a business as particular legal, taxation and risk management issues can arise.

If a trust is going to carry on a business, it is often best establish a company owned by the trust to undertake the business and for the trust to receive dividends from the Company. The Company then becomes one of the trust’s investments.

How does the trustee make decisions?

The trust deed can provide that the decisions of the trustees (if more than one) must be unanimous or may only require a simple majority of the trustees for it to be binding.

If the trust deed does not make a specific provision, the trustees’ decisions must be unanimous. Most trust deeds also provide that trustees’ decisions must be made or ratified in writing.

If a company is the trustee, the direction can decide how they will make decisions.

Terminology

A beneficiary is a person, company or other entity who can receive distributions from a trust.

A distribution is a payment from a trust to a beneficiary and may be part of the income and/or capital of the trust.

An enduring power of attorney appoints another person to act on your behalf if you are not able to make decisions. This power can apply to your property and your personal care and welfare or to both areas.

You forgive a debt when you formally acknowledge that all or part of the debt owing to you does not need to be repaid. This is a gift and needs to be recorded in writing.

You make a gift when you transfer a personal asset to another person or entity and receive no payment in return. You make a gift to a trust by directly transferring assets to the trust or by forgiving all or part of a debt the trust owes to you.

A gifting programme is a series of gifts that transfer your personal assets to a trust by way of regular gifts. These are normally made in a way so they do not become liable for gift duty.

A protector is a person who is not a beneficiary or a trustee and whose approval is required for specified trustee decisions.

A memorandum of wishes is a written summary of the goals and objectives for a family trust.

A settlor is the person who created the trust by transferring assets to the trustee subject to the provisions of the trust deed.

A sham trust arises where a trust deed has been signed and assets have been transferred to the trust but the settlor and trustees have practically ignored the concept of the trust and continued to treat all of the assets as the settlor’s personal assets.

A trust deed is the legal document that contains the set of rules for the operation of the trust.

A trustee is a person or body appointed by the settlor to hold legal title to the trust assets for the benefit of the beneficiaries. A trustee has legal control or the trust assets and must administer the trust in accordance with the trust deed. An independent trustee is a trustee who is not a beneficiary.

The trust income is the money the trust makes from the investment of its capital. It can include interest, rent, dividends and trading profits.

Trust capital is the assets of the trust and can include real estate, bank deposits, fixed interest and share investments.

A will is a legal document which sets out how a person wants their personal assets to be administered and distributed after their death.